The latest on Energetic and renewable energy trends.

Energetic Insurance Helps Redaptive Secure $50 Million Credit Facility from Rabobank

Energetic Insurance has played a key role in helping Redaptive, a San Francisco-based Energy-as-a-Service provider, secure a $50 million credit facility from Rabobank. By providing a unique credit insurance structure, Energetic has enabled Redaptive to finance over 1,000 energy efficiency projects, supporting growing demand from commercial and industrial (C&I) customers to reduce energy consumption.

This partnership allows Redaptive to diversify its credit counterparties and access lower-cost capital, advancing energy efficiency solutions in the market.

Read more about this innovative financing deal here.

What Changes to Expect in the Renewable Energy Industry in 2023

Developers, sponsors, financiers, and industry experts recently gathered in Austin, Texas for the Proximo US Power and Renewables Finance 2022 conference. Market participants were aligned on one overarching topic; change is coming to the renewable energy industry.

Cautious optimism in a time of industry transition

Attendees and speakers alike conveyed long-term optimism, primarily driven by the passing of the Inflation Reduction Act (IRA) and continued commitments by governments and large corporations to transition to renewable energy. Given the previous lack of new incentive legislation, the IRA was heralded for providing more certainty in the 10-year development horizon. Expanded and new incentives will yield continued and magnified investment in project development. Government incentives for renewable energy have attracted new capital to the sector, bringing with it the need for investor education, along with the unique problem of finding a way to efficiently deploy the influx of funds.

Positive tailwinds driving the industry forward were met with short-term questions around the impact of the broader macroeconomic environment, and what the interplay between the two opposing forces may yield. Heard throughout the event was the affirmation that projects set to close in 2022 should remain on track, subject to minor repricing. More emphasis was placed on forecasts around the 2023 funding market. Despite the aforementioned influx of capital into the energy transition, the short-term availability of capital could get tighter. However, the expectation is that market liquidity will still be available in 2023.

There seems to be an expectation that the renewable industry will see multiple operating entities aim to acquire funding via the public equity markets. This shift in funding sources may impact how developers weigh the benefits of retaining ownership of sites themselves, as opposed to building to sell. Interestingly, there is a belief that these deals will be viewed by the broader equity markets as growth investments rather than traditional dividend paying entities. Along with many other financial markets, the IPO market will likely remain dormant through the end of the year. But be on the lookout for deals to come into the public eye early to mid 2023.

How will projects be impacted?

Inflation concerns continue to be top of mind for those worried about the cost of debt and cost of materials. It would be hard to find a developer who did not have their own set of concerns regarding supply chains and the potential impact on existing projects. Fortunately, the resounding consensus was that the worst case was comprised of delays and repricing, not outright cancelation. Most industry experts expect the IRA to fundamentally alter the industry supply chain, but the specifics of how that will occur have yet to be fully fleshed out. The expectation is that domestic manufacturing will increase. However, the timing, scope, and magnitude of domestic manufacturing investments are yet to be determined.

Distributed generation (DG) was a key focal point. Multiple panelists either alluded to, or forecasted outright, an increase in the flexibility of DG structures and a move away from flat power purchase agreement (PPA) prices to a more dynamic way to limit basis risk in these deals.

This prognostication for increased complexity naturally comes with an increase in the level of forecasting and underwriting difficulty. The ratings agencies represented implied comfort with the harnessing of multiple methodologies for risk quantification. There still remains a gap between project developers’ view of risk and the methodologies used to underwrite distributed generation offtake at lending institutions. It is also expected to take time for new investors and sources of capital to become familiar with the renewable energy sector and the inherent risk/return dynamics.

The impacts of credit quality and role of insurance

Investors in the energy transition, new and longstanding, share the desire to mitigate investment risk. Risk drivers and risk mitigants are increasingly a topic of conversation. Developers and investors want to ensure viable project economics, long-term project performance, and reliable offtake demand.

Energetic’s own Jim Bowen took to the stage with others from the insurance industry to discuss the multiple avenues project participants can harness to get deals done more efficiently. Alongside Jim, Jeffrey Abramson, CFA of AXA XL, Jamie Brache of Vantage Risk Companies, Eric Popien of Atlantic Global Risk, Martin Bernstein of LBBW, and Donnie DiCarlo of BPL Global, discussed how insurance should be thought of as a financial product to improve funding terms and distribute risk. They explained why insurance should not be viewed as a mandatory boiler plate product needed to get a deal done, but a way to beneficially spread and share risk.

Panelists emphasized the level of customization involved in each deal and the value clients can gain from a relationship with an insurer. Insurers can get involved earlier in the project lifecycle to help creatively structure deals to make them work for all stakeholders, as opposed to buying and selling vanilla products in the open market.

Have questions on how Energetic Insurance can help improve project economics? Contact us here.

This article does not constitute and is not intended by Energetic Insurance to constitute financial advice or a solicitation for any insurance business.

The Good and Bad News on Renewable Energy & Environmental Tax Credits

Successful financiers and developers are always striving to better understand investment and underwriting risks in the context of long-term political and economic scenarios.

That is precisely what was at the core of the forward-thinking dialogues at the Novogradac 2022 Spring Renewable Energy and Environmental Tax Credits Conference in Denver. The well-attended forum outlined the latest industry trends, emerging technologies, and tax credit equity pricing and financing strategies.

Leading experts weighed in with a mix of bad and good news.

The Bad News:

The market is currently facing significant headwinds. Current law phases down solar Investment Tax Credits (ITCs) and Production Tax Credits (PTCs). In the absence of new legislation, Solar ITCs will drop to 22% by 2023, and the PTC expired at the end of 2021. Unfortunately, the Senate draft of the Reconciliation Bill was stalled by Senator Manchin in December 2021, and its prospects look bleak in this mid-term election year.

Further, the market has been anxiously awaiting the results of a Commerce Department investigation into possible circumvention of duties which could result in more solar tariffs. Jeremy Woodrum, Director of Congressional Affairs, Solar Energy Industries Association (SEIA) is hoping for a statement from Commerce by the end of August. Some of that anxiety was relieved by the Executive Order released after the conference on June 6th suspending new tariffs for the next two years.

Separately, JC Sandberg, Chief Advocacy Officer at American Clean Power (ACP) is advocating for a storage ITC. Storage is critical to a robust and resilient distributed energy system. A storage ITC could catalyze investment in much-needed battery infrastructure. Finally, ACP is also seeking streamlined local and Federal permitting.

The jury remains out on the state of and forecasts for the economy as a whole, and financial markets continue to be volatile. Interest rates are on the rise. Some commentators are predicting a 250-basis point hike over the course of the next year. Credit spreads are widening, and business confidence is wavering.

The Good News:

There is a lot of capital available to finance new projects, and in many ways it’s a seller’s market. Demand and supply are optimistically focused on the long-term. That being said, lenders are reviewing deals on a case-by-case and developer-by-developer basis. For example, some lenders remain cautious with respect to Low- and Moderate-Income (LMI) community solar given the perception of higher credit and subscriber churn risk. Others are wary of adding battery storage to projects as they are unable to assess the risks around re-charging. Nevertheless, offtake demand for renewable energy remains strong; utilities remain front and center and corporates are playing an ever-increasing role.

Solar currently accounts for only 4% of power generation in the US. If the US is to hit its 100 percent carbon-pollution free power by 2035, by 2031, more solar must be installed annually than has been installed cumulatively through 2021, according to SEIA.

Bottom Line:

Investment in clean energy cannot slow – it must increase and accelerate. Successful financiers and developers should pay attention to macro-economic, regulatory, and ESG-related trends and forecasts. They should carefully plan, build partnerships, and harness emerging tools, technologies, and approaches that allow them to ramp distributed energy investments.

The market continues to explore insurance - credit, panel supply, performance, regulatory, and trade – as a tool critical to enabling the achievement of domestic energy goals.

Energetic is proud to be at the center of this drive. Our credit insurance products enable broader and more cost-effective capital provision by covering sub-IG and unrated offtakers in a wide array of renewable energy markets.

Economic and political rough seas are ahead. The strongest players in energy financing know not to stall; they see this as an opportunity to plan and capture long-term market opportunities.

__________________________________________________________________________________

Thanks to Nathaniel Eng and the whole Novogradac team for organizing the event, and to Sam Kamyans and John Marciano at Allen & Overy, Julian Torres at Scale Microgrid Solutions, Rob Martorano at Greenskies Clean Energy, Dirk Michels at MidValley Power, Craig Robb at City National Bank, Evan Karambelas at Soltage, Rod Eckhardt at Seminole Financial Services, Justin Elswit at Celtic Bank, Winston Chen at Clean Capital, and many more for your insights and company.

__________________________________________________________________________________

Have questions on how Energetic Insurance can reduce barriers to cost-effective procurement and help support the greening of supply chains? Reach out!

This article does not constitute and is not intended by Energetic Insurance to constitute financial advice or a solicitation for any insurance business.

How the Inflation Reduction Act is Impacting Clean Energy Financing and Development

The Inflation Reduction Act (IRA) was front and center two weeks ago at Novogradac's Renewable Energy conference. We entered the event with several questions - many were answered, but as we peel back the onion, even more questions emerge.

There is no doubt that the IRA will bring about a favorable investment environment across the renewables spectrum, but there is still a lot of dust that needs to settle.

Here are three things we learned:

1. Everyone is waiting for IRS guidance

Getting that guidance could take up to a year. The IRA offers investors 10 years of certainty around tax treatment, but as always, the devil is in the details. As guidance emerges from the IRS, the devils will be revealed, but it will take a long time before anything binding is issued. This bill represents the first time that workforce protections and content requirements have been attached to tax incentives. That, coupled with the sheer size and scope of the bill, lead us to believe that guidance will be slow to emerge.

2. Direct Pay and Transferability will have limitations

Direct pay is useful but is limited to a narrow set of circumstances - tribal lands and other tax-exempt entities. The main winner of direct pay is the manufacturing sector, which will be able to benefit from direct pay to stimulate working capital investment. Similarly, transferability will likely be more limited than initially thought - at least in the near term. IRS guidance will certainly help add clarity, but there remain numerous nuances to consider.

3. Up to 70% of the capital stack in tax equity!

Given the amount of tax equity now available, many are asking whether there is a place for debt in the capital stack. The answer across the conference was a resounding yes, and not just because most of the attendees were bankers. Getting to 70% tax equity requires taking advantage of every adder available, which is unrealistic. The thought does leave us with two unanswered questions:

(1) Will lenders relax their sponsor equity requirements?

(2) If lenders are seeing their ticket sizes drop in favor of tax equity, will they need to identify ways to expand their appetite or addressable market in order to deploy the same capital volume? Time and IRS guidance will likely reveal an answer.

If you have thoughts on likely impacts of the Inflation Reduction Act, reach out or leave your thoughts in the comments.

We’ll keep you posted as we learn more.

November 2022 Monthly Market Commentary

This is a series of monthly market commentaries and updates from Energetic Insurance. It was wonderful to see so many of you over the last 3-4 months across various conferences. The energy within the industry is at an all-time high! While we are all awaiting official guidance around the Inflation Reduction Act (IRA), it has not slowed the IRA from being a focal point throughout the industry. We look forward to sharing our take on the IRA and the insights we've been hearing from the market with you soon. In the meantime, we are sharing other news we have been following below.

Market Updates

Highlighted themes include the evolving credit risk landscape, climate news, and the banking regulatory environment. Summarizing the articles below:

- Credit Risk: 1/3 of U.S. Small Businesses are unable to pay rent in full (Alignable); Rising Default Rates (Swiss Re)

- Climate News: State of the Market: Renewables Procurement, Scope 3, and Carbon Credits (Energetic Insurance)

- Regulatory Environment: Inflation Reduction Act Shines a Bright Light on Renewable Energy, but Guidance is Needed (Novogradac)

Over one-third of U.S. small businesses unable to pay full rent in October, survey shows (Alignable)

"In September, rent delinquency was at a six-month low, as optimism for Q4's earning potential was high and some small business owners reported increased sales. But a month later, 37% of U.S. small business owners could not pay their rent in full and on time in October." Read the full article here.

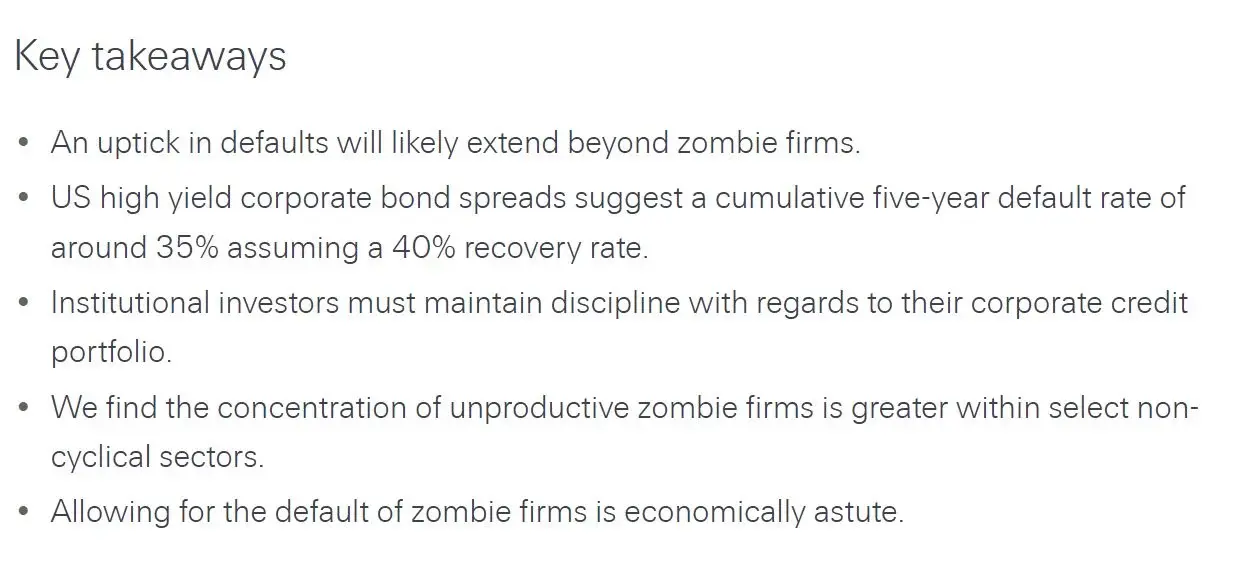

Rising defaults: "zombie firms" will be the first to fall (Swiss Re)

The rate of corporate defaults is likely to increase. In a severe recession scenario, a high yield default rate of around 15% - last seen during the global financial crisis – is possible. Read the full article here.

State of the Market: Renewables Procurement, Scope 3, and Carbon Credits (Energetic Insurance)

The market is ill-prepared to meet the insatiable demand for clean energy and other footprint-reducing solutions prompted by unprecedented SBTi, net zero, or other ESG commitments. The renewables market has shifted from a buyer’s market to a seller’s market. Credit presents a significant barrier to scaling clean energy procurement. Scope 3 is the next frontier, and credit issues are likely to be magnified greater when attempting to green supply chains. Keep reading for our key takeaways. Read the full article here.

Inflation Reduction Act Shines a Bright Light on Renewable Energy, but Guidance is Needed (Novogradac)

“There is so much more opportunity to use these credits because of the Inflation Reduction Act,” said Matt Meeker, a partner in the Dover, Ohio, office at Novogradac. “The IRA will have a big impact. We just don’t know exactly how to monetize it yet.” Read the full article here.

Energetic Insurance, Credit Insurance featured as Renewable Energy Strategy Tool (ENGIE Impact)

In a recent webinar, ENGIE Impact engaged with experts from Seminole Financial Services, Nexamp, and Energetic Insurance to discuss ways to prioritize renewable energy strategy while reducing costs. Credit insurance is featured as a means to significantly drive down buyers’ overall costs and reduce the support needed to establish creditworthiness for unrated companies, subsidiaries, or those with sub-IG credit ratings. Learn more here.

Join Our Team

New job alert! We are hiring for a Head of Sales. This role comes with a great balance of direction and autonomy. You will join as a senior leader in an exciting startup revolutionizing the cleantech and insurance industries. You will be the driving force behind our sales team as Energetic Scales rapidly. This is an opportunity to use your skills for good as you help support clean energy projects and unlock financing for an untapped market. See opportunities here. Reach out to kathryn@energeticinsurance.com with interest.

Until Next Time

Be sure to follow our company LinkedIn page for more updates on the evolving commercial credit landscape, as well as news about Energetic. If you would like to submit any projects for a rapid price quote, you can do that here.

State of the Market: Renewables Procurement, Scope 3, and Carbon Credits

GreenBiz and the Clean Energy Buyers Association (CEBA) convened climate action leaders in San Jose for VERGE22 and CEBA Connect last week.

Everyone from clean energy developers, to buyers, financiers, and advisors were aligned on one thing; the market is ill-prepared to meet the insatiable demand for clean energy and other footprint-reducing solutions prompted by unprecedented SBTi, net zero, or other ESG commitments. Keep reading for our key takeaways.

Corporate demand for clean energy is insatiable

Renewables procurement was top-of-mind for many of those in the audience. Thanks to programs like RE100, hundreds of businesses have committed to relying on 100% renewable energy. Procurement challenges are an unintended result as clean energy development fails to keep pace with rapidly growing demand. Businesses are competing to procure renewable energy, especially via virtual power purchase agreements (VPPAs). The winning bidders are primarily large investment-grade corporates. A huge swathe of the market remains unserved.

The renewables market has shifted from a buyer’s market to a seller’s market

Demand has outpaced supply. Developers are racing to satiate demand, while navigating ongoing supply-chain challenges, rising interest rates, lengthy interconnection and permitting queues, and more. The majority of buyers are toiling with how to successfully procure renewable energy as most of the market is unrated or sub-investment grade, including those procuring energy through third-party platforms, on behalf of franchises, or via subsidiaries.

Credit presents a significant barrier to scaling clean energy procurement

According to the Clean Energy Buyers Association, “only 23 percent of the most mature U.S.-listed companies have sufficient credit ratings to support the development of large-scale offsite clean energy projects.” Lauren Tatsuno from 3Degrees, Harry Singh of Goldman Sachs, and Brooke Malik of Apex Clean Energy spoke to four common, but imperfect solutions; leveraging existing banking relationships, credit sleeves, posting high amounts of credit, and PPA terms flexibility. Developers, buyers, financiers, and advisors emphasized the limited success they have had with these approaches, the persistence of credit barriers, and the need for more solutions.

Scope 3 is the next frontier

Those lucky enough to be able to tackle their scope 1 and 2 emissions are now increasing their focus on scope 3 emissions. Approximately 80-90% of overall emissions stem from supply chains. These emissions fall outside of the direct control of procuring entities, yet they fall within the scope of influence. Supplier engagement, education, and enablement are key. Only a fraction of companies are actively engaging with their supplier base today in an effort to decrease emissions. Entities like OneTrust provide footprint calculating tools and are working with procurers and suppliers to make reporting easier. Companies like Meta have developed support programs for their suppliers. These programs are critical for ESG success as approximately 98% of Meta’s emissions stem from scope 3 from their many suppliers providing building materials, technology for data centers, professional services, and more. Suppliers most often begin with renewable energy procurement, employee training, and energy efficiency programs. Unfortunately, credit barriers resurface here, too, as an estimated 70%+ of suppliers for major corporations are sub-investment grade or unrated. Panelists acknowledged that financing is a key barrier for suppliers. Without targeted financing and credit support, a minority of suppliers will be able to address even their scope 1 and 2 emissions.

Carbon credit investments are ramping

As the mitigation hierarchy teaches us – those in a position to eliminate and reduce emissions should do so, and then consider the role carbon offsets can play in mitigating their remaining footprint. Corporates, startups, NGOs, scientists, multilateral public and private institutions are endeavoring to bring clarity, guidance, and liquidity to carbon markets. Innovators, registries, and verifiers are focusing on how to deliver high-quality nature-based and engineered carbon credits. Early adopters are already purchasing credits or making commitments. Most prospective buyers are keeping an eye on carbon market movements, while first improving the efficiency of their operations, electrifying where they can, and procuring clean electricity to the maximum extent possible.

Collaboration is critical

The structural market challenges present in clean energy and efficiency markets cannot be solved unilaterally. We were pleasantly overwhelmed by requests for support and collaboration. Buyers need credit support. Developers need more affordable financing. Financiers need more projects to invest in. Advisors need tools in their kits to support buyers when they run into procurement barriers. Our team at Energetic Insurance solves alongside developers and financiers every day. We are increasingly interested in hearing directly from buyers and supporting their procurement needs.

_________________________________

Have questions on how Energetic Insurance can reduce credit barriers, support cost-effective renewable energy procurement, and help support the greening of supply chains and reduction of scope 3 emissions? Contact us here.

This article does not constitute and is not intended by Energetic Insurance to constitute financial advice or a solicitation for any insurance business.